When buying or selling a business, the transaction is usually structured either as a share sale or an asset sale. Both methods are widely used in corporate transactions and can achieve similar commercial outcomes, but they differ in:

- legal structure;

- risk allocation;

- tax treatment; and

- practical complexity.

In a share sale, the buyer acquires ownership of the company itself by purchasing its shares. In an asset sale, the buyer acquires selected business assets without taking ownership of the company entity. Each approach has advantages and limitations depending on the parties’ objectives, risk appetite, and transaction context.

Businesses commonly compare these options based on:

- scope of transfer (company vs selected assets);

- liabilities assumed by the buyer;

- tax and pricing implications; and

- transaction complexity and due diligence requirements.

This article explains the key differences between share sales and asset sales to support informed decisions when structuring a business sale.

Comparison Table

| Feature | Share Sale | Asset Sale |

| Pricing | May be discounted to reflect inherited liabilities or risks | Often reflects value of selected assets without full liability exposure |

| Best for | Selling or acquiring an entire business as a going concern | Buying or selling specific business divisions or assets |

| Key Features | Buyer acquires company shares and inherits all assets and liabilities | Buyer acquires selected assets and may avoid most liabilities |

Overview of Share Sale

A share sale is a transaction in which a buyer acquires sufficient shares in a company to obtain ownership and control. By purchasing the shares rather than individual assets, the buyer effectively steps into the position of the previous owners. The company continues operating as before, but under new ownership.

Additionally, parties commonly choose share sales when the seller seeks a complete exit and the buyer accepts the company’s historical obligations in exchange for continuity and a simpler transfer.

| PROs | CONs |

| Transfers the entire business without needing to assign individual assets | Buyer inherits all known and unknown liabilities |

| Seller can achieve a clean break after completion | Extensive due diligence is usually required |

| Business continuity is preserved for employees and customers | Price may be reduced to reflect assumed risks |

| Often regarded as more tax-efficient than asset sales | Shareholder approvals may be necessary |

Call 0808 196 8584 for urgent assistance.

Otherwise, complete this form, and we will contact you within one business day.

Overview of Asset Sale

An asset sale is a transaction in which a buyer acquires specific business assets rather than the company itself. The buyer can select which assets and rights to purchase, such as:

- equipment;

- intellectual property;

- contracts; or

- goodwill.

Unlike a share sale, ownership of the company does not change. The seller continues to own the corporate entity and any assets or liabilities not transferred. This enables both parties to clearly define what the transaction includes.

Buyers often use asset sales to acquire only part of a business or to avoid taking on the company’s historic liabilities.

| PROs | CONs |

| Buyers can choose specific assets and avoid most liabilities | Transfer process can be legally complex |

| Lower risk exposure compared with acquiring the entire company | Individual assets may require formal assignment steps |

| Due diligence is typically narrower and shorter | Seller may retain unwanted liabilities |

| Seller can retain parts of the business | Often less tax-efficient than share sales |

- Office for National Statistics, Mergers and Acquisitions involving UK Companies: October to December 2025.

Who Should Choose Share Sale or Asset Sale?

You may choose a share sale if you:

- want to buy or sell the entire business entity;

- prefer continuity of contracts, employees, and operations;

- seek a clean exit as a seller;

- are prepared to assume historic liabilities (as buyer).

You may choose an asset sale if you:

- want to acquire or dispose of only part of a business;

- prefer to limit exposure to past liabilities;

- want flexibility in selecting assets or excluding obligations;

- intend to retain certain business components after sale.

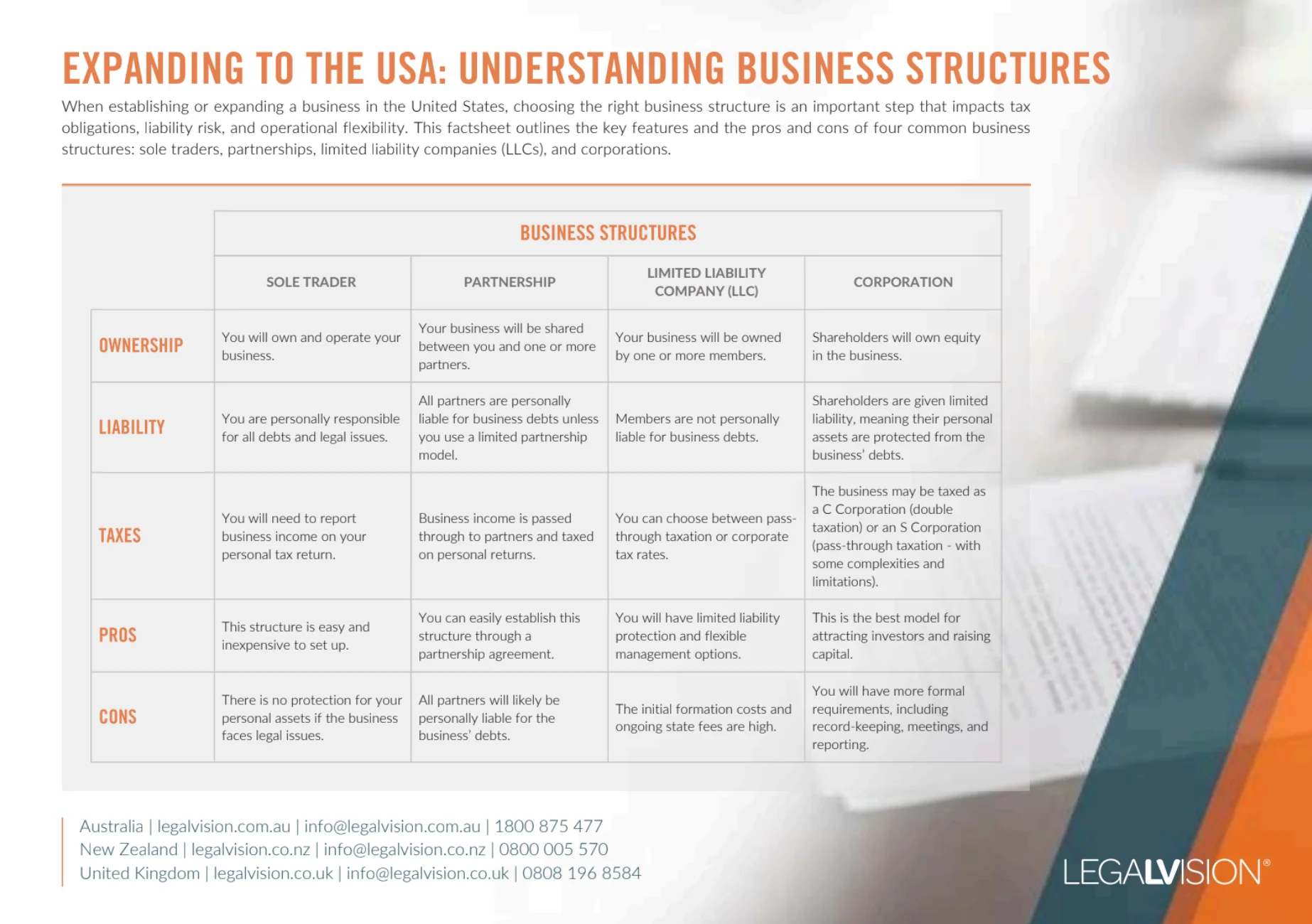

This factsheet outlines the key features and the pros and cons of four common US business

structures: sole traders, partnerships, limited liability companies (LLCs), and corporations.

Key Takeaways

Parties use share sales and asset sales as two established methods to transfer business ownership or value. Moreover, A share sale transfers the company itself, including all assets and liabilities, while an asset sale transfers selected assets without changing company ownership.

The appropriate structure depends on:

- transaction scope;

- risk allocation;

- tax considerations; and

- commercial objectives.

LegalVision provides ongoing legal support for businesses through our fixed-fee legal membership. Our experienced business lawyers help businesses manage contracts, employment law, disputes, intellectual property, and more, with unlimited access to specialist lawyers for a fixed monthly fee. To learn more about LegalVision’s legal membership, call 0808 196 8584 or visit our membership page.

Frequently Asked Questions

What is the main difference between a share sale and an asset sale?

A share sale transfers ownership of the company, including all assets and liabilities. An asset sale transfers selected assets only, with the seller retaining the company and remaining liabilities.

Which structure carries more risk for the buyer?

A share sale generally carries more risk because the buyer inherits all existing and potential liabilities. An asset sale allows the buyer to limit liability exposure.

Which option is more complex to complete?

Asset sales are often more complex because parties must transfer or assign each asset individually. Share sales are usually simpler from a transfer perspective.

Which structure is more tax-efficient?

This depends on the circumstances, but share sales are often more tax-efficient for sellers, while asset sales may have different tax implications for both parties.

We appreciate your feedback! Request your free consultation now.